Budget Breakdown: 35-Year-Old Project Manager Making $114,000 in San Diego

How a 35-year-old Project Manager can finish building an emergency fund and decide what financial freedom actually looks like

Today I am budgeting for a 35-year-old Project Manager living in San Diego, CA making $114,000 per year.

They are earning a great salary and value putting their money towards travel and saving.

Their top financial goals are:

Fully fund their emergency fund

Determine what to do with a $19k inheritance

Save in a taxable brokerage for future flexibility (down payment, sabbatical, starting a business, etc)

Let’s dive in!

💸 Want a chance to be featured in a future Budget Breakdown? Submissions are available to paid subscribers.

Current Budget

Income

After taxes and payroll deductions, they take home $5,772 per month. This is their base take-home for their expenses and savings goals.

Retirement

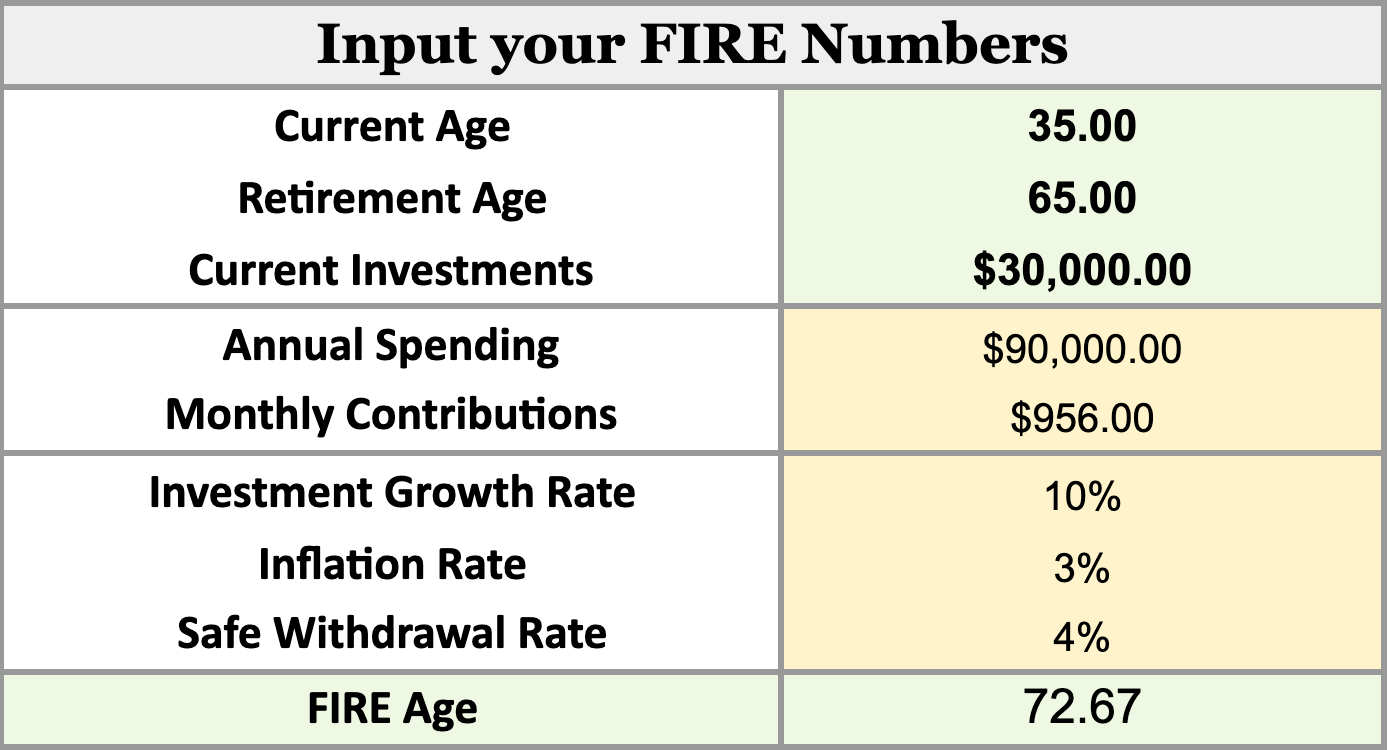

They currently have $30,000 saved for retirement. They max out their Roth IRA every year and put around $331 in their 401a (there is an additional $351 going towards a 401a loan payback. We will ignore this for now as the loan is at an 8% interest rate). Their goal is to retire at 65 with an annual spend of about $100,000/year.

She also has a pension, which gives us a lot of stability and flexibility here. We will lower our annual expenses by $10,000 to account for this on the low end.

At their current contribution rate of $956/month, they are on track to retire around age 73.

To hit their goal of retiring at 65 they need to increase their investment contributions by around $870 per month.

Budget

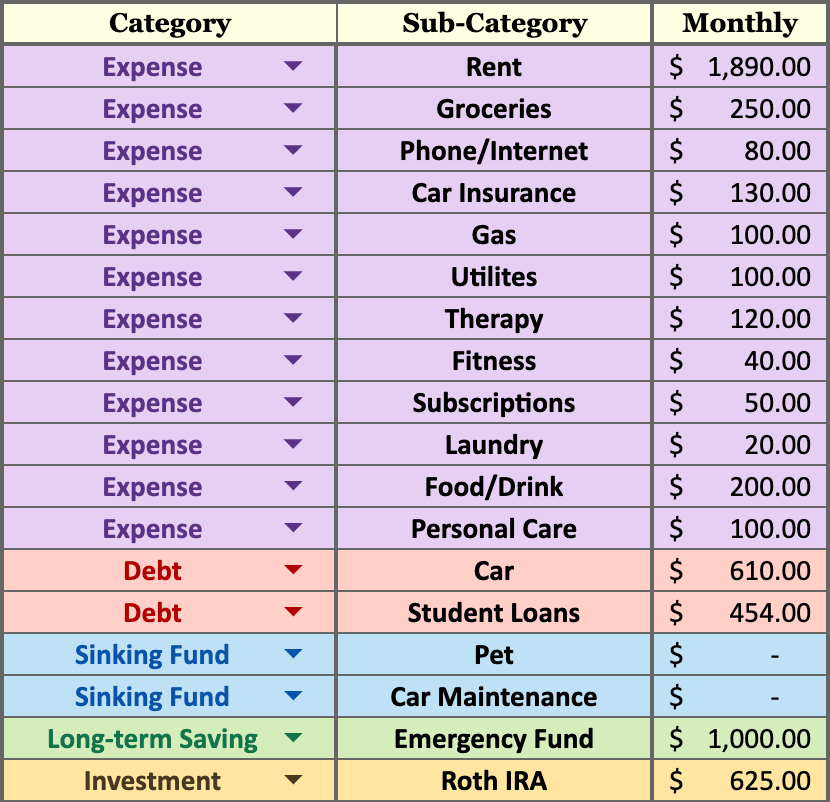

Rent at $1,890/month is the largest fixed expense and honestly reasonable for San Diego, one of the most expensive rental markets in the country.

Beyond that, their budget is pretty lean.

In terms of debt, they currently have a car loan at 5.64% and 36 months left on the loan. They also have $76,000 in student loans at 3.61-6.35% APR — $454/month in minimum payments.

They are pursuing Public Service Loan Forgiveness (PSLF), which forgives the remaining federal student loan balance after 120 qualifying payments (10 years) while working for a qualifying public service employer. They currently have 7.25 years until forgiveness and plan to stay at their current employer the entire duration.

They will essentially pay back what they borrowed and have the rest wiped clean. This is an extraordinary benefit and the single most important thing to know about their student loans is this: do not pay extra.

Every extra dollar paid toward these loans is a dollar that would have been forgiven anyway. Stay the course, make the minimum qualifying payments, and let PSLF do its job. The best thing they can do is verify they are on a qualifying repayment plan and that their employer certifies their employment annually.

The 3 Key Budget Changes I Recommend

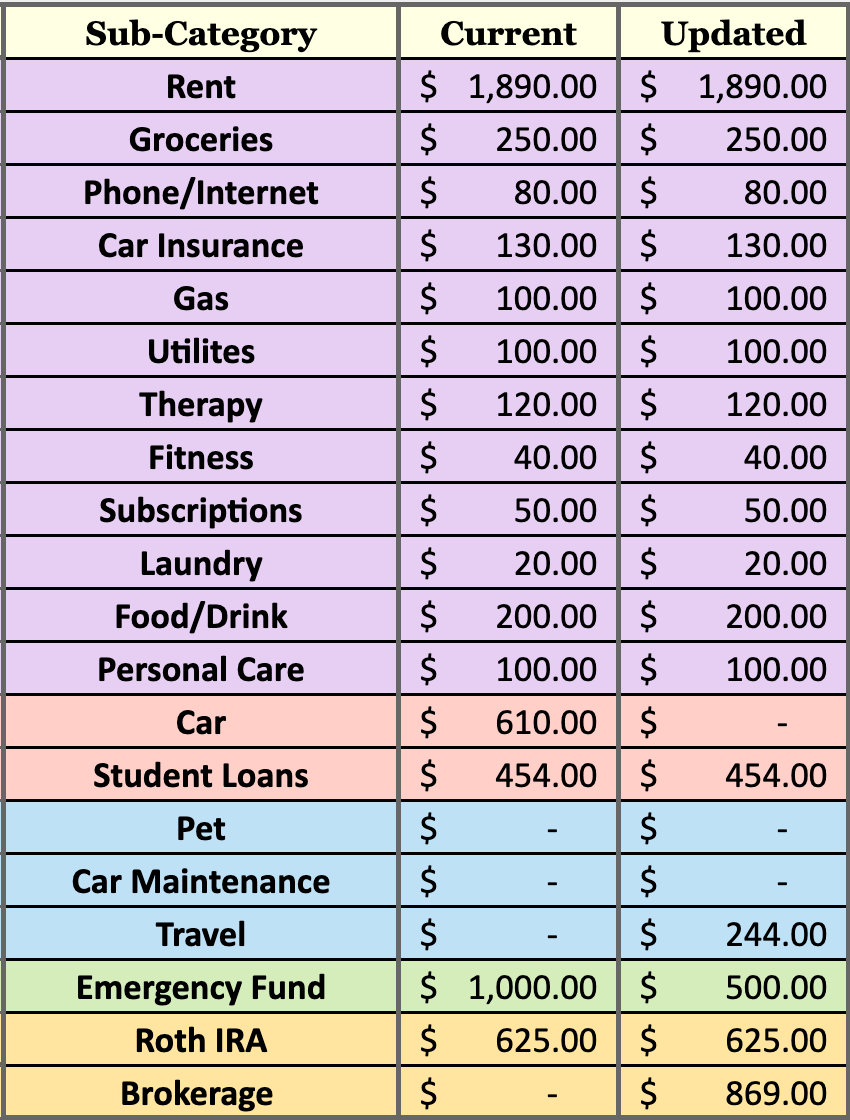

1. Contribute to Emergency Fund consistently, but not aggressively

They feel stable in their job, so while we will make progress each month towards the emergency fund, this is not our #1 priority.

They currently have $8,000 saved and we will want to build to a full 6 month emergency fund, which is around $25,000.

If we save around $500 per month we will hit this goal in 3 years! (The car loan will also be paid off, but we will keep the $25,000 goal to account for any increases in expenses).

2. Pay off car loan with inheritance

With their $19k inheritance they will be able to fully pay off their $19k car loan and free up $610 per month.

Now I am typically team invest over debt payment if the debt is under 7% interest, BUT when I ran their numbers it made more sense to provide cash flow flexibility.

If we invested the full amount, they would need to invest $1,700 per month to hit the goal of retirement at 65. However with their cash flow they could only afford to invest $1,459.

If we paid off the car loan instead, they would need to invest $1,825 per month, $125 more. But with their freed up cash flow they can easily afford it!

3. Create a travel sinking fund

There is an important piece missing from this budget. Travel!

They mention it’s a priority but we aren’t setting anything aside for it.

We will make sure to invest $1825 per month to get them to their FIRE age of 65, and the leftover $244 will go right to travel.

Updated Budget

They are in a really good place with their budget. We are being very conservative with their pension, not factoring in social security, and their 401a contributions will increase once they fully payback their loan. I believe they will have a good buffer in their taxable brokerage for taking a sabbatical or starting a business.

Now it’s a matter of staying the course and being disciplined with their budget!

Want to map out your own plan?

Friendly neighborhood disclaimer: I am not a licensed financial professional and this is not financial advice. These are the changes I would personally make based on assumptions and the limited data I have received. Please do your own research and work with a professional for your unique situation.

I can’t believe I’m saying this, but $250/mo seems low for groceries!

I love reading these! Thanks for sharing your thoughts and budgeting tips!