Budget Breakdown: 32-Year-Old Adjunct Instructor Making $50,000 in Denver

How a 32-Year-Old adjunct instructor can manage their $50k income and prepare for upcoming student loan payments

Today I’m budgeting for a 32-Year-Old adjunct instructor living in Denver, CO earning $50,000 a year.

They’re working what is essentially a full-time job without the benefits to show for it, while simultaneously finishing a full-time master’s program.

Their top financial goals are:

Pay off all credit card debt

Build their emergency fund to 3–5 months of expenses

Have room for some extra spend such as generous tips, eating out occasionally, and a monthly massage for pain management

They value putting their money towards housing, food & dining, health & wellness, travel, and savings.

Let’s dive in!

💸 Want a chance to be featured in a future Budget Breakdown? Submissions are available to paid subscribers.

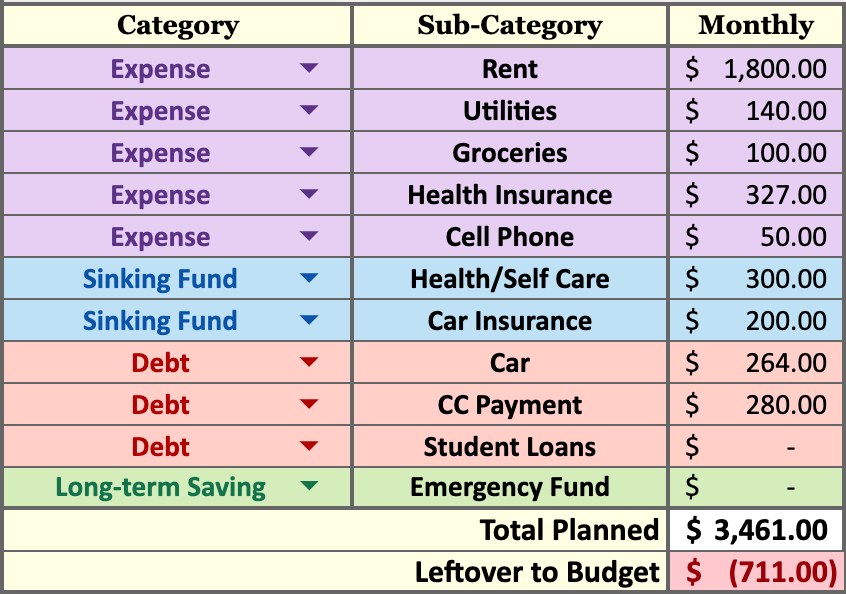

Current Budget

Income

After taxes, they take home $2,750 per month from their adjunct position to allocate towards their expenses.

Retirement

They currently have $0 saved for retirement and are contributing $0/month. Their goal is to retire at 60 with $65,000/year in spending. At their current contribution rate, retirement at 60 is not on the table.

They would need to invest $1,685 per month to retire by 60, and $1,155 per month to retire by 65.

However, retirement contributions are not the priority right now.

The priority is finishing their degree, managing their health, and getting a higher paying position.

Once they land a full-time position after graduation, that is when they will be able to start making a huge difference in their retirement and their debt. A full-time industry role with benefits and a retirement match would completely transform what is possible here.

Budget

At $1,800/month, rent is eating 65% of take-home pay before a single other bill gets paid. Add on the car payment, car insurance, health insurance, Lyme treatment, utilities, cell phone, and credit card payments.. and expenses alone come to approximately $3,161/month.

Here is our debt breakdown:

Credit card: $7,000 (assuming around 22-30% APR) — $280 minimum payment

Student loans: $118,000 at 4–14% APR — minimum payments beginning in approximately 6 months

Car Loan: Unknown — $264 monthly payment

This budget is in the red on bare minimums alone, including a $280 credit card minimum that is hardly moving the needle on $7,000 in high-interest debt. Health insurance is climbing to $500 next year, and student loan payments on $118,000 of debt will begin within six months. There is no wiggle room here, which is exactly why we need a clear plan before those changes arrive.

One note is that their Groceries are extremely low at $100 per month. This is because they started a meal prep business. While it has not yet turned a profit, they are seeing a drastic reduction in their grocery bill.

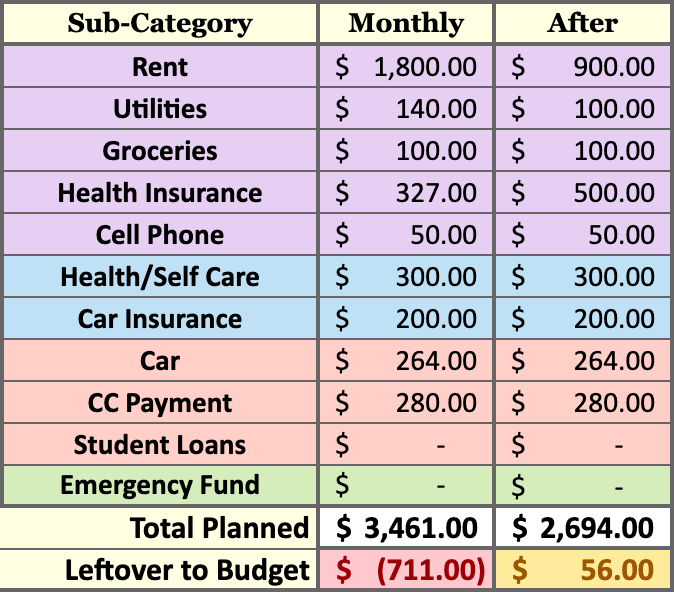

The 3 Key Changes I Recommend

1. Get a Roommate to Cut Rent

This is the most impactful change available in this entire budget.

If they can find a roommate and bring rent and utilities down to $900/month that frees up $900/month, which is transformational at this income level.

I completely understand this isn’t always easy or desirable. Denver’s rental market is competitive, and sharing space has real lifestyle costs. But this budget does not have another lever of this size.

2. Understand their upcoming student loan payment

They need to understand what they owe on their student loan since this is coming up quickly.

I have a guide below ↓

Student Loans Got a Major Overhaul. Here's What to Do Next.

Big changes just hit federal student loans. Like, BIG. And I’m not going to make you figure it out from a government website alone.

3. Understand that this is a moment in time

Managing a disease like Lyme disease while going to university and working is a huge feat.

The priority here is getting out of the red as fast as possible so the credit card debt doesn’t spiral out of control.

They don’t need to do 1000 side hustles and burn themselves out even more, they just need to get through this period of time until they can land a full-time position with benefits.

I would love to redo this budget once they land that position!!

Updated Budget

Increased income, a 401(k) match, and health insurance will move this whole plan forward dramatically.

Until then they need to focus on getting a roommate, understanding their upcoming student loan payments, and taking care of their health.

Want to map out your own plan?

Friendly neighborhood disclaimer: I am not a licensed financial professional and this is not financial advice. These are the changes I would personally make based on assumptions and the limited data I have received. Please do your own research and work with a professional for your unique situation.