Budget Breakdown: 23-Year-Old Software Engineer Making $107,400 in Seattle

How a 23-Year-Old software engineer is balancing aggressive investing with lifestyle goals like travel and saving for their next car

Today I am budgeting for a 23-year-old Software Engineer living in Seattle with one roommate earning $107,400 per year.

They value putting their money towards Food & Dining, Travel, and Savings, which tells me they are trying to strike the balance between enjoying life now and setting themselves up for the future. At only 23, they have already built a financial foundation that many people do not reach until much later in their career.

Their top goals are:

Max out their Roth IRA

Max out their HSA

Save for buying a car within the next 2–5 years

Let’s get into the details!

💸 Want a chance to be featured in a future Budget Breakdown? Submissions are available to paid subscribers.

Current Budget

Income

After taxes and payroll deductions, they’re working with $5,178/month to allocate across their budget.

Retirement

They are already investing heavily, contributing consistently to a 401(k), Roth IRA, and HSA.

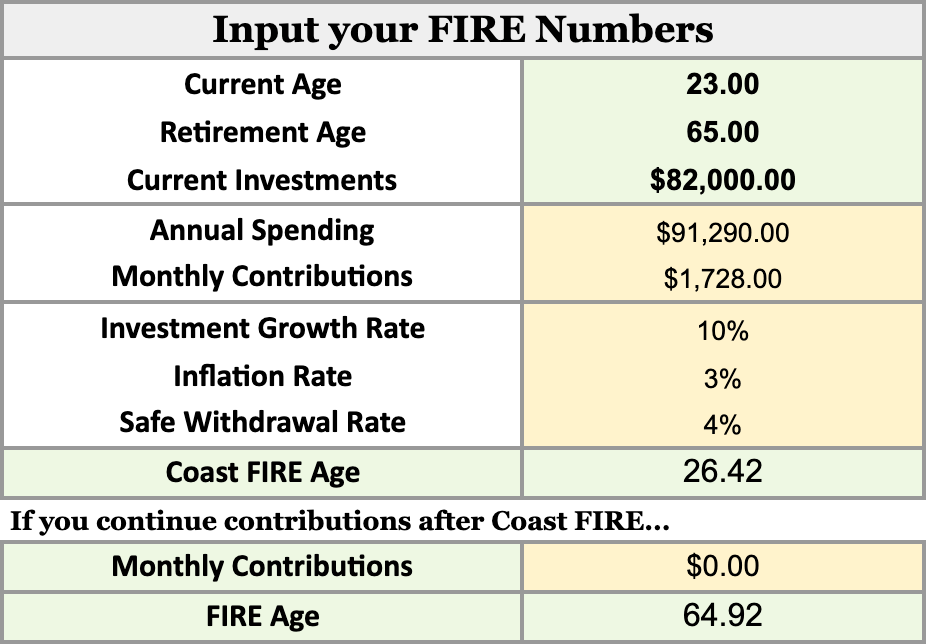

They already have about $82,000 invested, which is extremely impressive for someone who is only 23 years old.

Their goal is to retire around age 65, spending about $91,000 per year in retirement. Starting this early gives them a huge advantage thanks to compound growth.

At their current savings rate, they are projected to reach Coast FIRE in less than four years, which is incredible.

Budget

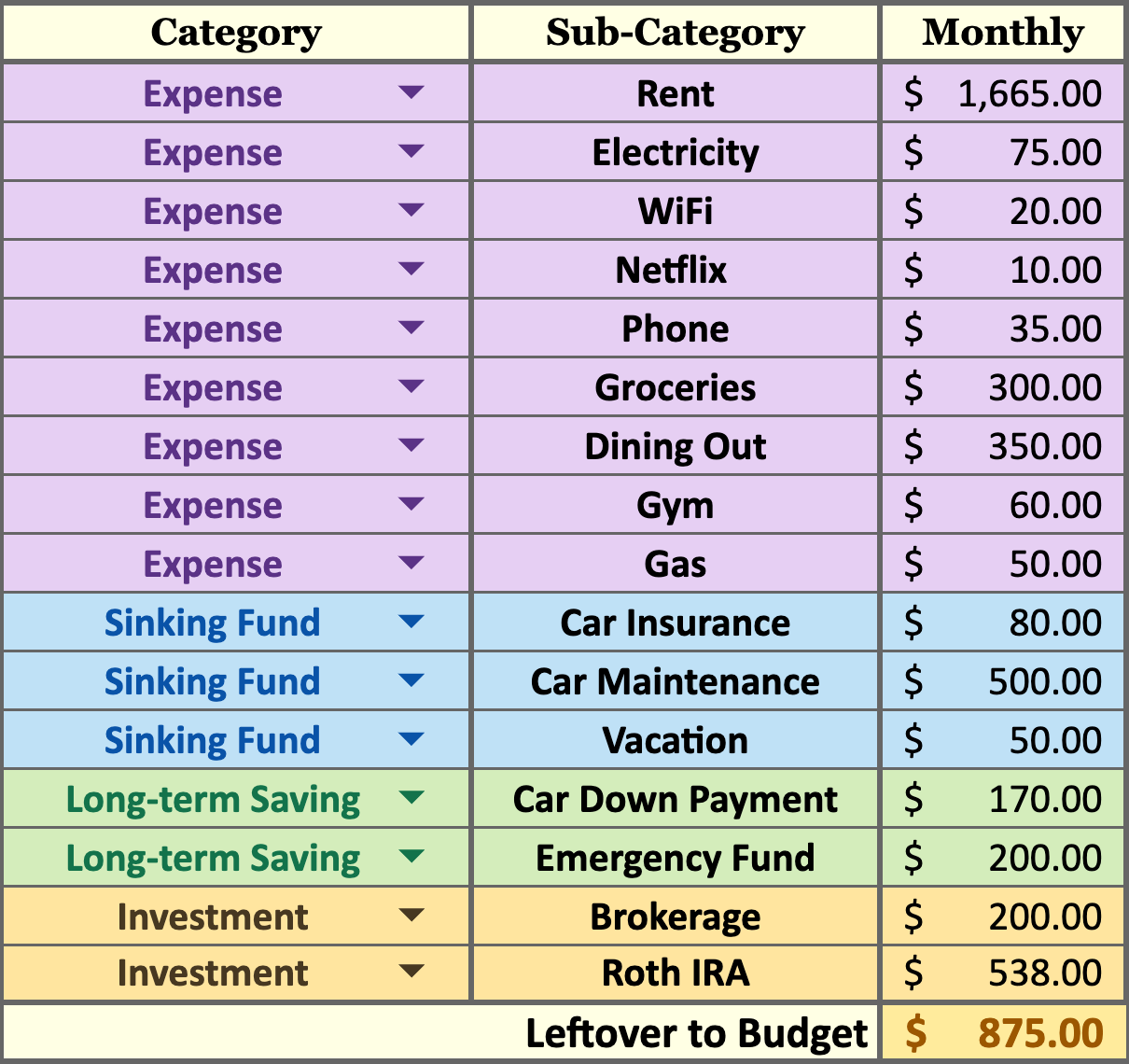

Their expenses are very reasonable for living in Seattle, especially while splitting housing with a roommate. Rent comes in at $1,665/month, which keeps their largest expense manageable and allows them to continue prioritizing savings and investing.

Outside of housing, the rest of their spending stays relatively balanced. Groceries, utilities, and subscriptions remain modest, while dining out reflects one of the areas they value most.

They also contribute consistently to several sinking & savings funds, including savings for car maintenance, insurance, a future car purchase, and travel. Setting aside money each month for these expenses helps prevent surprises and keeps their budget stable throughout the year.

However one piece of the budget that is concerning is $500 per month towards car maintenance. This is $6,000 per year. I’m wondering what the heck is going on here (this is probably why they are saving for a new car lol).

The biggest advantage in this budget is that they currently have no debt, which allows a large portion of their income to go directly toward investing and future goals.

Overall, this is a very strong financial foundation with controlled spending and an impressive savings rate for someone just starting their career.

The 3 Key Budget Changes I Recommend

1. Max Out Roth IRA and HSA Contributions

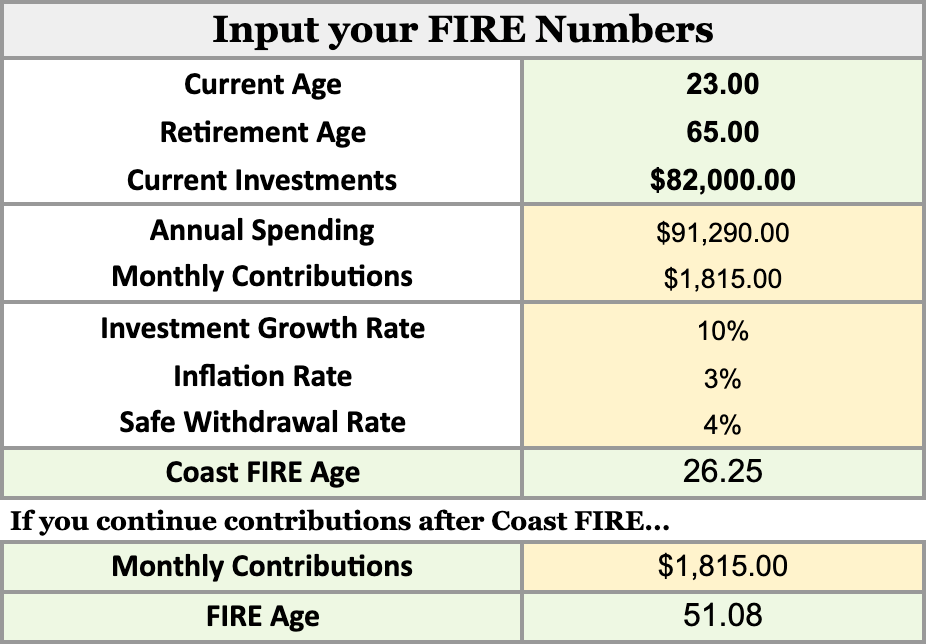

One of their main goals is maximizing their tax advantaged accounts, so the first step is updating contributions to match the 2026 contribution limits.

Their Roth IRA contribution should increase to $625/month

Their HSA contribution should also increase to $366/month

These accounts provide some of the best tax advantages available, and maximizing them early can significantly accelerate long-term wealth building.

If they continue to invest after hitting Coast FIRE, they could potentially retire as early as 51!

2. Increase Savings

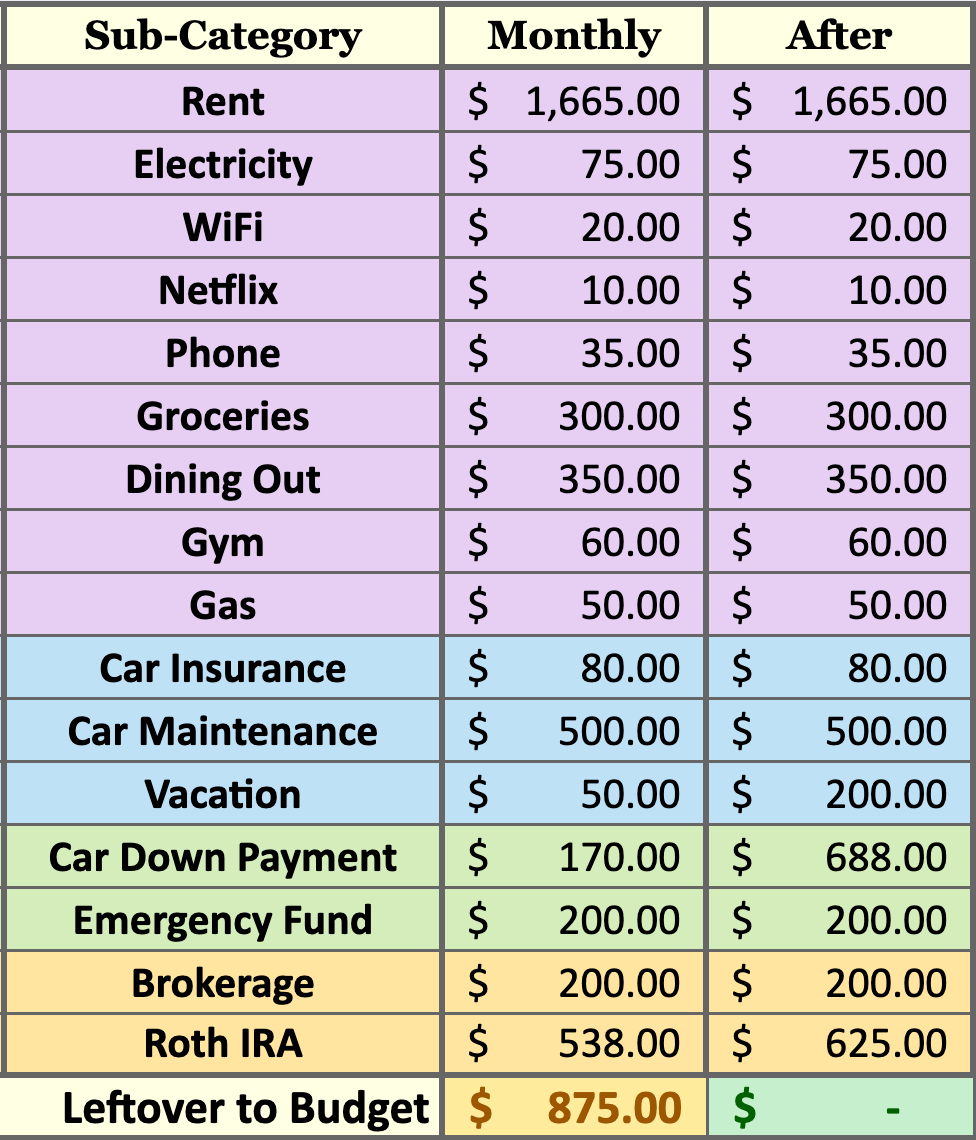

Buying a car is one of their major goals within the next 2–5 years. Right now they contribute $170/month toward a car down payment, but since they already save heavily in other areas, I would increase this fund to about $688/month.

At this savings rate, they could potentially buy their next car with cash instead of taking on a loan. Avoiding a car payment early in life can free up hundreds of dollars each month that could instead be invested or redirected toward other financial goals.

Hopefully this new car also drastically reduces their Car Maintenance fund as well.

3. Increase Travel Budget

Travel is one area they value, but their current travel sinking fund sits at only $50/month.

With their strong savings rate and lack of debt, there is room to increase this category to about $200/month so they can enjoy more experiences now while still staying on track with their financial goals.

Building lifestyle spending around the things they truly value helps make their financial plan more balanced and sustainable long term.

After they finish saving for their new car, I personally would put that extra money towards fun (since they are so ahead of their investment goals).

Updated Budget

At 23 years old, they are already in an incredibly strong financial position. The main focus now is simply optimizing where their money goes so it aligns with both their long term goals and the lifestyle they value.

Want to map out your own plan?

Friendly neighborhood disclaimer: I am not a licensed financial professional and this is not financial advice. These are the changes I would personally make based on assumptions and the limited data I have received. Please do your own research and work with a professional for your unique situation.